Key Observations

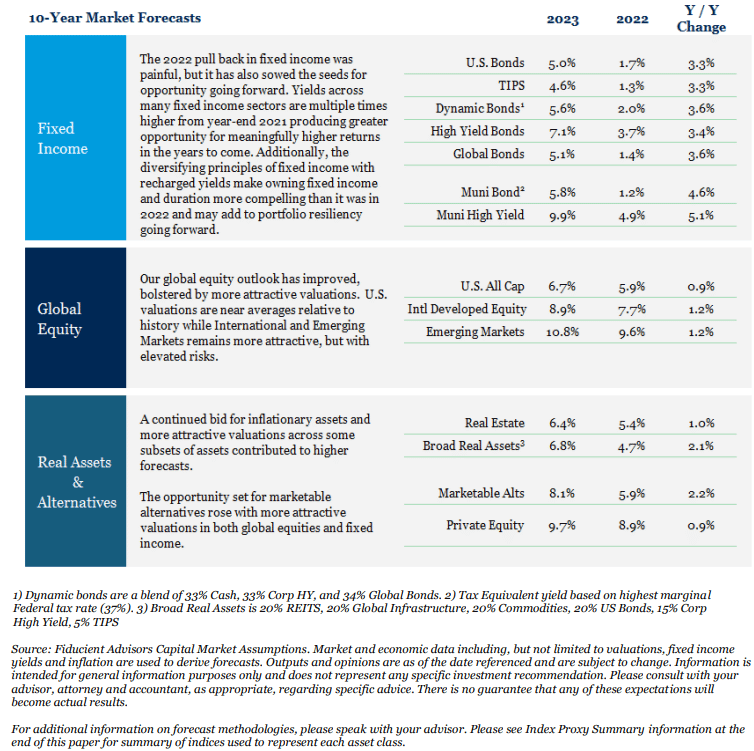

- Our capital market forecasts increased across all asset classes, most materially in fixed income given the change in yields over 2022.

- The three themes we see driving the market, Persistent Volatility, Moderating Inflation, and a Bear Market Bottom, will come to life over different time periods in 2023 and beyond.

- Year-over-year we are adding to high quality fixed income and high yield primarily by reducing dynamic bonds and increasing U.S. mid and small caps from U.S. large caps. We

- remain modestly underweight to non-U.S.

Our investment views are based on a simple idea: as facts change, so may our outlook. The last few years have been an interesting period for this ethos as our annual outlook is beginning to feel like a game of ping-pong, oscillating between bulls and bears, as the environment shifts around us. Our 2021 outlook discussed optimism as the proverbial economic doors swung open as COVID eased. Our 2022 outlook moved in the other direction, calling for volatile markets based on (among other factors) persistent inflation, the Fed stepping on the economic breaks and market valuations and expectations set for perfection. In this outlook, Goodbye TINA (there is no alternative), we find ourselves on the other side of the market pendulum, seeing greater opportunity in 2023 albeit amidst a period of considerable uncertainty. Our outlook is tempered with humility and pragmatism, recognizing the future remains uncertain, as it always has. However, as the market dynamics have changed so have our opinions and we are excited to share our view for 2023 and beyond.

2023 Themes

Rarely do market themes fit neatly into a calendar year and 2023 is no exception. However, there are three distinct themes in markets today which we believe are likely to unfold over varying time periods. Therefore, our views are presented as if they were three acts of a play. The first act is one in which changes are just beginning and will have long-term implications yet to be fully appreciated. The middle act is one in which change is obvious, but the resolution is not imminent. In the final act, we believe events are more likely to take place in the near term.

First Act: Persistent Volatility

In the first act of a play, facts and circumstances are often revealed about a character which in time will shape their path, but careful attention needs to be paid to see how these early clues may shift their trajectory. We view the reversal of zero-bound interest rates and the unraveling of globalization as those pivotal moments leading to higher long-term volatility for both stocks and bonds.

The last 10+ years in markets have been unique compared to long-term history. One could describe markets since the Global Financial Crisis as having low interest rates, low inflation and low growth coupled with maximum accommodation and maximum liquidity. These conditions have led to abnormally low volatility and have encouraged additional risk taking or TINA, the acronym for “there is no alternative” (to owning more equity). We believe that reversing some, but not all, of these conditions may produce higher structural volatility across multiple asset classes. Additionally, these shifts may also mean that investors expecting the playbook of the last 10 years to be the same for the next 10 may be disappointed.

Portfolio Impact

Resiliency, risk management and humility all come to mind as important components of allocations. As a

result, our 2023 allocations include increased exposure to high-quality and intermediate-duration

U.S. fixed income. While fixed income has lacked its historical diversification benefits in 2022, we believe

with recharged higher yields and greater volatility in equity markets, fixed income may retake its historical

position of diversifying equity exposure. Additionally, while valuations would compel us to increase our allocation to non-U.S. equity, we are holding our year-over-year allocation flat based on the greater potential for exogenous events outside of the United States. Non-U.S. equity remains attractive but risk management compels us to temper that view.

Middle Act: Moderating Inflation

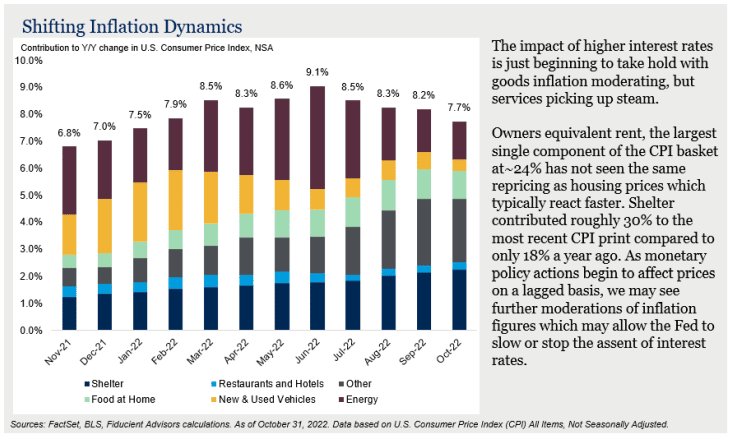

In the middle of the play, rising conflict is obvious, but the resolution has yet to take hold. These inflection points often leave the audience uneasy about the future. Inflation, and the Fed’s role in moderating it, is in its middle act. It is unlikely the curtain will drop on inflation in 2023 falling straight to the Fed’s target of 2%. However, that is not what is required for a market bottom or for the Fed to pause. We simply need the path to resolution to be illuminated. So, while inflation may moderate over the years to come, its pivotal moment in market sentiment may be closer at hand.

Portfolio Impact

The good news/bad news of inflation moderating, but not immediately, highlights our points above regarding resiliency. The path is unlikely to be smooth, but seemingly in the right direction. We increased our real asset allocations coming into 2022 and we plan to maintain that increased position in light of inflation remaining above the Fed’s 2% target.

We are adding Treasury Inflation Protected Securities (TIPS), a financial asset that acts a lot like a

real asset. The market is hyper focused on short-term inflation but is seemingly complacent about long-term inflation, leaving room for opportunity in the middle. Such an allocation to high-quality inflation-linked bonds adds quality to the portfolio and potential upside if long-term inflation assumptions are too sanguine.

Final Act: Bear Market Bottom

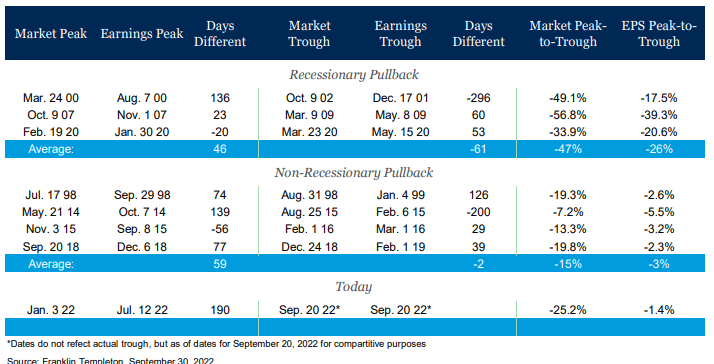

In the final act, we fully grasp the conflict and perhaps even see what is necessary for resolution but are uncertain quite how it will play out. We believe we are in a similar place with markets bottoming. Let’s first build context around bear markets. Since 1950, the average pullback of 20% or more has lasted approximately 14 months; the longest of these was 31 months from March 2000 to October 2002. The shortest drawdown was less than two months in 2020. While there is no such thing as an average bear market, with history as a guide, our 11-month-old bear market is likely closer to its end than its beginning.

Now, how do bear markets typically unfold? The most common pattern is multiple contraction. This leads

markets lower first, then the Fed ends a hiking cycle or begins an easing cycle and finally, earnings and

expectations fall, creating a new base from which to build healthy forward expectations.

Index prices can be broken down into two primary components, earnings per share (EPS) and multiples. EPS is the economic value created by businesses and what investors are buying. Multiples are how much an investor is willing to pay for those earnings. Multiples are often driven by sentiment and are one of the first things reflected in prices. Corporate earnings, on the other hand, are backward-looking. Moreover, the impacts on businesses from higher interest rates and/or slowing demand takes time to appear in financial statements. Therefore, the typical pattern of bear markets is multiple contraction first, leading the market lower, followed by earnings.

This has certainly been the case in 2022. Multiple contraction has accounted for more than 100% of the pullback as earnings remain modestly positive so far in 2022. The question remains, what role will earnings play in the market bottoming this time around?

As shown in the table, there is a meaningful difference in the earnings impact in recessionary versus nonrecessionary environments. Our expectation remains that if a recession takes place, it will be a modest and cyclically led recession rather than one driven by structural imbalances like during the Global Financial Crisis or an exogenous factor like COVID-19.

With that in mind, second and third quarter earnings are beginning to reflect a potential modest economic contraction. In fact, second quarter earnings ex-energy were down 4.0% (up 6.2% with energy) and third quarter earnings with 99% of companies reported show earnings ex-energy down another 5.0% (up 2.5% with energy) [1]. Why ex-energy? Russia’s invasion of Ukraine propelled commodity prices up, pushing earnings for the sector up 137.31 % year-to-date. This is unique to the energy sector and is not reflective of the rest of the market. All of this compares to earnings expectations (as late as June of this year) of 10.8% earnings growth for third quarter 2022.[2] These lofty expectations were a potential source of volatility as reality may not be as rosy and that has proven to be the case. All in, earnings are beginning to reflect the economic reality of a moderating economy. This is a healthy step forward for a bear market bottom and again suggests we are nearer the end than the beginning.

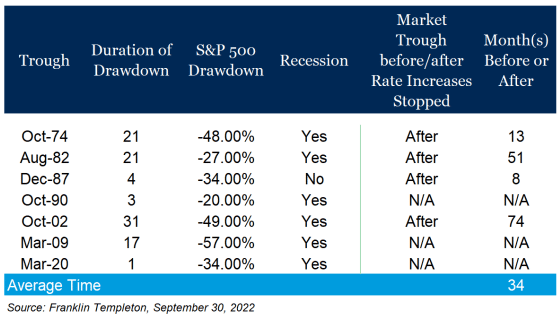

Finally, what role does the Fed play in all of this? To no surprise, given the Fed focus this year, an important one in our view. History has shown us markets tend to bottom after the Fed is done raising rates. Intuitively this makes sense. If the Fed is raising rates, they are proactively looking to cool economic activity.

Yet given their dual mandates of price stability and full employment, the operative word is cool, not kill. When the Fed sees modest success in controlling inflation they will stop or pause. However, the full effect of higher rates takes some time to work through businesses and markets. It is a bit like turning the shower handle to change the temperature: you have to wait a second to see if you got it right. Therefore, businesses are often amidst contraction when the Fed stops increasing rates. It is certainly conceivable that the market bottoms before the Fed officially stops as it tapers back from 0.75% moves to 0.50% or less. However, the market is less likely to bottom if the Fed is accelerating or maintaining its hawkish stance.

Portfolio Impact

We have no ability, or need, to precisely call the market bottom. However, as we look forward, we believe it prudent to prepare for a potential market rebound. As such, we are increasing our weighting to U.S.

small cap stocks and high yield bonds, recognizing they have historically led over large cap and

investment grade bonds respectively in rebounds.

Additionally, a less hawkish Fed following a market bottom may moderate U.S. dollar strength and prove to be a tailwind for non-U.S. equity. But based on the greater potential for exogenous events outside of the United States we do not plan to increase our non-U.S. equity exposure.

Final Thoughts

2022 was the reset button for many markets. Exiting zero-bound interest rate policies, moderating inflation and repricing global fixed income and equity have all helped sow the seeds for a brighter outlook in 2023 and beyond. While we anticipate volatile asset prices will persist in the years to come, leaning into newly created opportunities may prove to be the right decision over the long-term.

This report is intended for the exclusive use of clients or prospective clients (the “recipient”) of C.W. O’Conner Wealth Advisors and the information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of C.W. O’Conner Wealth Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on C.W. O’Conner Wealth Advisors research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.

Disclosures and Index Proxies

This report does not represent a specific investment recommendation. Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and are reported gross of any fees and expenses. Any

forecasts represent future expectations and actual returns; volatilities and correlations will differ from forecasts. When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise notes. Each index is unmanaged, and investors can not actually invest directly into an index:

INDEX DEFINITIONS

FTSE Treasury Bill 3 Month measures return equivalents of yield averages and are not marked to market. It is an average of the last three three-month Treasury bill month-end rates.

Bloomberg Capital US Treasury Inflation Protected Securities Index consists of Inflation-Protection securities issued by the U.S. Treasury.

Bloomberg Muni 5 Year Index is the 5 year (4-6) component of the Municipal Bond index.

Bloomberg High Yield Municipal Bond Index covers the universe of fixed rate, non-investment grade debt.

Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

FTSE World Government Bond Index (WGBI) (Unhedged) provides a broad benchmark for the global sovereign fixed income market by measuring the performance of fixed-rate, local currency, investment-grade sovereign debt from over 20 countries,

FTSE World Government Bond Index (WGBI) (Hedged) is designed to represent the FTSE WGBI without the impact of local currency exchange rate fluctuations.

Bloomberg US Corporate High Yield TR USD covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

JP Morgan Government Bond Index-Emerging Market Index (GBI-EMI) is a comprehensive, global local emerging markets index, and consists of regularly traded, liquid fixed-rate, domestic currency government bonds to which international investors can gain exposure.

JPMorgan EMBI Global Diversified is an unmanaged, market-capitalization weighted, total-return index tracking the traded market for U.S.-dollar-denominated Brady bonds, Eurobonds, traded loans, and local market debt instruments issued by sovereign and quasi-sovereign entities.

MSCI ACWI is designed to represent performance of the full opportunity set of large- and mid-cap stocks across multiple developed and emerging markets, including cross-market tax incentives.

The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Russell 3000 is a market-cap-weighted index which consists of roughly 3,000 of the largest companies in the U.S. as determined by market capitalization. It represents nearly 98% of the investable U.S. equity market.

Russell Mid Cap measures the performance of the 800 smallest companies in the Russell 1000 Index.

Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the US and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country

The Wilshire US Real Estate Securities Index (Wilshire US RESI) is comprised of publicly-traded real estate equity securities and designed to offer a market-based index that is more reflective of real estate held by pension funds.

Alerian MLP Index is a float adjusted, capitalization-weighted index, whose constituents represent approximately 85% of total float-adjusted market capitalization, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis.

Bloomberg Commodity Index (BCI) is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the

commodity, sector and group level for diversification.

Treasury Inflation-Protected Securities (TIPS) are Treasury bonds that are indexed to inflation to protect investors from the negative effects of rising prices. The principal value of TIPS rises as inflation rises.

HFRI Fund of Funds Composite is an equal-weighted index consisting of over 800 constituent hedge funds, including both domestic and offshore funds.

Cambridge Associates U.S. Private Equity Index (67% Buyout vs. 33% Venture) is based on data compiled from more than 1,200 institutional-quality buyout, growth equity, private equity energy, and mezzanine funds formed between 1986 and 2015.

HFN Hedge Fund Aggregate Average is an equal weighted average of all hedge funds and CTA/managed futures products reporting to the HFN Database. Constituents are aggregated from each of the HFN Strategy Specific Indices.

Goldman Sachs Commodity Index (GSCI) is a broadly diversified, unleveraged, long-only composite index of commodities that measures the performance of the commodity market.

Material Risks Disclosures

Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

Cash may be subject to the loss of principal and over longer period of time may lose purchasing power due to inflation.

Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impact by currency and/or country specific risks which may result in lower liquidity in some markets.

Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

Private Equity involves higher risk and is suitable only for sophisticated investors. Along with traditional equity market risks, private equity investments are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility

and/or the potential loss of capital.

Private Credit involves higher risk and is suitable only for sophisticated investors. These assets are subject to interest rate risks, the risk of default and limited liquidity. U.S. investors exposed to non-U.S. private credit may also be subject to currency risk and fluctuations

Download our 2025 Financial Planning Guide