Recessionary Resilience – Defying Expectations

Key Observations

- In our 2023 Outlook, Goodbye TINA, we outlined three broad themes that were likely to influence markets in 2023 – continued volatility, moderating inflation and a bear market bottom. The first half of 2023 has largely validated those views and we do not anticipate material changes ahead of year end rebalancing.

- Our portfolio positioning remains similar, and we believe our exposure to Treasury Bonds, in particular, adds to the resiliency of our portfolios while also benefiting long-term returns based on higher overall yields.

- While many anticipated a recession in 2023, one has yet to materialize. Our view is that while the risk of a recession is rising, attempting to time its occurrence is often unproductive. By positioning portfolios to weather potential risks associated with economic contractions, we can navigate these downturns more effectively and avoid the pitfalls often found with market timing.

Off to an Interesting Start

Despite one of the most anticipated recessions in U.S. history, we sit here halfway through the year defying those predictions even in the face of developing geopolitical risks, a banking crisis (remember that?) and the Federal Reserve (Fed) continuing to raise rates. If 2023 has yet to humble those who seek to time the market, perhaps they missed that the S&P 500 was up 16.9% in the first half of the year and the technology-driven NASDAQ advanced an impressive 32.3%.[1]

If we were to wrap up 2023 now and evaluate our themes for the year – continued volatility, moderating inflation and bear market bottom – we could declare victory. Admittedly, however, a deeper look into markets suggests that 2023 has not come to pass quite as we drew it up. An AI “revolution”, multiple banking failures across the globe and China’s cautious reopening were not part of our base case. That said, our allocations are neither built on short-term views nor reliant on getting every detail precisely right. So, as we lift our gaze toward the long-term, we remain confident our portfolio positioning remains consistent with maximizing the likelihood of our clients reaching their goals and we foresee no significant adjustments to our positioning for the remainder of the year absent significant changes occurring within the investing environment.

2023 Themes – Revisited

1. Continued Volatility

The landscape of the financial world has undergone a significant shift from the low-rate, low-inflation and low-growth environment of the past decade. We find ourselves in a new regime characterized by higher interest rates, increased inflation and uncertain growth prospects. In this transformed setting, we believe volatility will be more prevalent and this belief has been validated in the early months of 2023 with volatile interest rates, the substantial divergence between winners and losers in equity markets and varying macroeconomic conditions across the globe. The likely result is that asset allocation will hold greater significance than it has in recent years.

Portfolio Impact

Resiliency, risk management and humility were central tenants to our asset allocation coming into 2023 and we believe those elements remain critical. While we are confident we have our finger on the pulse of capital markets, we did not anticipate a regional banking crisis nor interest in AI becoming its own economic cycle.

Through mid-year, our additions to Treasury Bonds have helped guard against higher levels of risk and have performed in line with our expectations. Despite the persistently inverted yield curve, we will maintain our positioning as we approach the end of the year. Our belief that the Fed’s rate hiking cycle is nearing its conclusion, coupled with the possibility of economic growth slowing in the coming quarters, bolsters the importance of these positions within the context of broader portfolio construction considerations.

2. Moderating Inflation

Coming into 2023, our expectation was for a meaningful decline in inflation, even though we did not anticipate fully “solving” inflation and meeting the Fed’s target of 2%. Through the middle of the year that has certainly been the case. June Headline CPI reached 3%, down from a peak of 9.1% seen in June of 2022.[1] Beneath the surface of 3% CPI, there are additional positive indications. Shelter costs, which we discussed as a lagged input in our annual outlook, made up 91% of the 3% June CPI reading.2 If shelter CPI data catches up to real-time data, it is likely to continue to dampen the inflation outlook. Furthermore, nearer-term data continues to decelerate giving the Fed more flexibility in future policy. Over the last six months, “super core” CPI (CPI less shelter, food and energy) has risen by 2.8% on an annualized basis.3 These near-term inflation trends indicate even more progress than is reflected in the annual headline figures.[2]

Portfolio Impact

In 2023, we strategically initiated a position in Treasury Inflation-Protected Securities (TIPS) as part of our growing interest in high-quality intermediate-term debt and the attractiveness of this position relative to inflation expectations. As inflation has subsided and we enter what can be described as “the messy middle”, where inflation may fluctuate between 2% and 5%, we continue to believe exposure to real contractual returns and high-quality government debt through TIPS remains advantageous for overall portfolio construction.

3. Bear Market Bottom

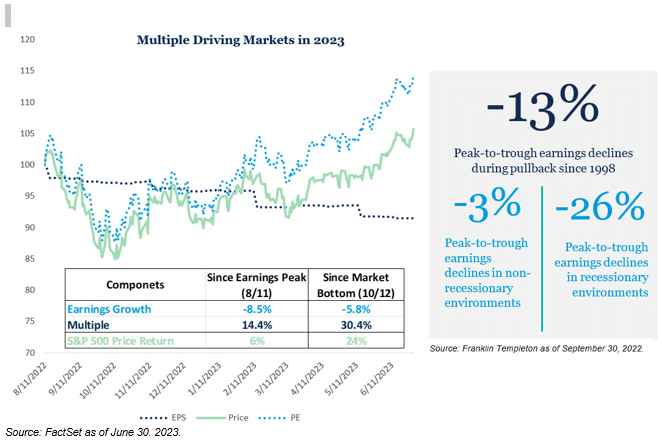

The actions taken by the Federal Reserve in 2022 to curb inflation played a significant role in driving down bond and stock prices. As we observe the Fed approaching the end of its rate hike cycle, we believe that investor focus should shift towards earnings as a key indicator for identifying the beginning of the next sustainable market rally. Earnings in the United States reached their peak in August 2022 and have since declined by -8.5% as of June 30, 2023.1 However, the market has rallied since October of 2022 largely based on investor’s willingness to pay more for stocks (higher multiples). Since the 1990’s, earnings have fallen peak-to-trough in market pullbacks on average -13%, with a range of -2% in the fall 2018 to -39% during the Global Financial Crisis.[3] Considering our view that any potential recession (more on that below) would be a

minor one rather than a major event, we have made significant progress in resetting the baseline for lower earnings upon which future growth can be built. The crucial question that remains is whether earnings will soon reach their bottom and begin to grow, justifying the higher multiples we are witnessing in the market today. Alternatively, it is possible that prices have expanded too rapidly, and multiples may need to contract in response to lower earnings.

Portfolio Impact

As we highlighted in our outlook earlier this year, we have no ability or need to precisely call the market bottom. That said, we deemed it prudent at the end of 2022 to prepare for prices to rise and indeed they have. Our position in high-yield bonds has yielded positive results to start the year. Nonetheless, our allocation to small-cap U.S. stocks has underperformed in comparison to their large-cap counterparts. This shortfall can be attributed to the disproportionate impact of the U.S. regional banking crisis on representative small-cap indices, coupled with the strong rally in mega-cap stocks driven by interest in artificial intelligence.

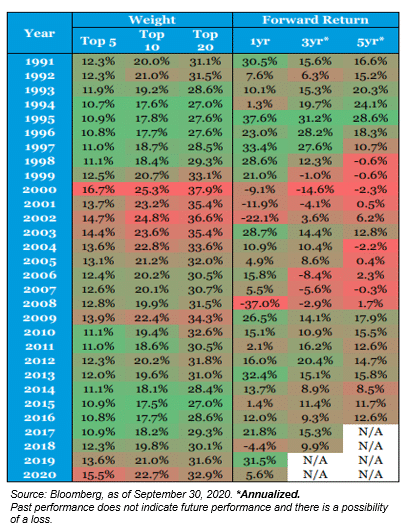

The rally witnessed in U.S. stocks has exhibited a somewhat unique characteristic, whereby a small number of securities have accounted for a significant portion of the overall return. Specifically , 56% of the rally in the S&P 500 can be attributed to just five stocks. To put it differently, more than 9% of the 16.89% return of the index was derived from these five securities.[1] This level of concentrated contribution surpasses the market rally observed in 2020, during which “stay-at-home stocks” disproportionately outperformed other securities.

, 56% of the rally in the S&P 500 can be attributed to just five stocks. To put it differently, more than 9% of the 16.89% return of the index was derived from these five securities.[1] This level of concentrated contribution surpasses the market rally observed in 2020, during which “stay-at-home stocks” disproportionately outperformed other securities.

It is crucial to recognize that narrow markets, characterized by concentrated leadership, can act as both a catalyst for upward movements, as witnessed this year, and for downward movements. We have observed since 1991 that markets with periods of narrow leadership often face greater challenges in the future. Intuitively, this makes sense, as upward momentum in the market becomes reliant on a small handful of securities.

This type of market leadership reinforces our previous statements regarding volatility and the importance of portfolio positioning that favors allocations capable of mitigating equity market risk.

Defying Recessionary Odds

There is a saying in market research, “analysis of averages leads to average analysis”. It appears many forecasters entering 2023 fell prey to this approach and based on historical recession data proclaimed with great confidence that 2023 was a recession year. However, no such recession has materialized, and the clock is running out in 2023. Our view remains the same as how we entered the year. The likelihood of a recession occurring in the foreseeable future is rising based on a growing body of forward-looking economic data showing the potential for slower future growth.

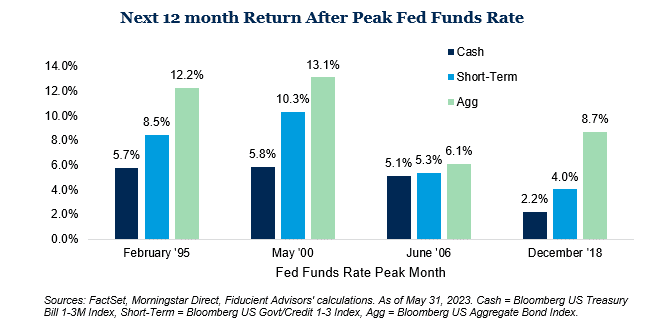

With that said, we have also written on the “recession red hearing”. Even if one could perfectly time recessions, markets tend to anticipate economic contractions both on the way down and the way up as shown in the accompanying chart. Recessions are a normal part of the economic cycle, and rather than fearing them, we believe in constructing resilient portfolios that embrace their inevitability. Moreover, it seems that investors have become conditioned to view recessions as catastrophic events akin to the global financial crisis or the COVID-19 pandemic. In reality, economic contractions and expansions are natural and healthy components of the economic cycle. Therefore, our allocation to risk assets overall and within asset classes anticipate and reflect these already embedded risks.

In closing, while 2023 has offered new opportunities and challenges we believe our long-term outlook and portfolio positioning remains the same as when we came into the year. For more information, please schedule a meeting, or contact any of the professionals at C.W. O’Conner Wealth Advisors.

[1]Morningstar Direct as of June 30, 2023

[2]U.S. Bureau of Labor Statistics as of May 31, 2023.

[3]Franklin Templeton as of September 30, 2022.

Disclosures & Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses.

- The S&P 500 Index is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Bloomberg US Treasury Bill 1-3M Index includes aged U.S. Treasury bills, notes and bonds with a remaining maturity from one up to (but not including) three months. It excludes zero coupon strips.

- Bloomberg US Govt/Credit 1-3 Index is the 1-3 year component of the U.S. Government/Credit Index, which includes securities in the Government and Credit Indices. The Government Index includes treasuries and agencies, while the credit index includes publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity, and quality requirements.

- Bloomberg US Aggregate Bond Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Material Risks

- Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and over longer period of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

Download our 2025 Financial Planning Guide