Markets Heat Up in July

Favorable economic data fuels risk assets as markets post solid gains during July 2023.

Key Observations

- Markets posted favorable returns in July as investors found renewed optimism in economic data being reported, even in the face of year-over-year earnings declines.

- The Federal Reserve raised rates in July, now targeting 5.25-5.5% for the Fed funds rate. Markets have all but priced in a pause at this level for the remainder of the year.

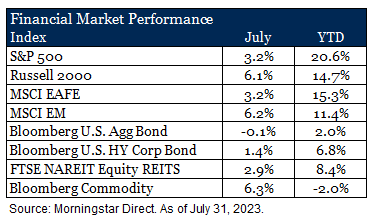

Market Recap

Financial markets were hot in July, starting the second half of the year off with a bang. There was a clear appetite for riskier segments of the market as equities generally outperformed fixed income. Even in the face of negative year-over-year earnings growth so far for the second quarter, favorable economic data helped bolster returns. The U.S. economy grew by 2.4% in the second quarter according to the advance estimate from the BEA and inflation continued to moderate as well, with year-over-year CPI touching 3% in June. U.S. equities performed well, posting mid-single digit returns. Small capitalization stocks (Russell 2000 Index) outpaced large cap companies (S&P 500 Index) during the month, driven in large part by strong smaller regional bank performance relative to large money center banks. Non-U.S. markets also posted favorable returns, with both developed and emerging markets in positive territory. Emerging regions (MSCI Emerging Markets Index) fared better than developed (MSCI EAFE Index) on the back of strong performance from China, Columbia and South Africa. Europe, however, lagged as the region continues to grapple with sluggish economic activity and higher inflation.

Market Review – July 2023

Fixed income was mixed as interest rate volatility remained. Ultimately the U.S. 10-year Treasury yield ended the month at 3.97 %, 16 basis points higher than it began. The seemingly favorable economic backdrop and appetite for risk helped propel longer yields higher, while the Federal Reserve increased the federal funds rate another 0.25 percentage points (now targeting 5.25-5.50%), pushing short-term rates up. The propensity for risk played out in the bond market as well as corporate high yield posted a positive return, supported by stronger than anticipated economic data. Diversifying areas of the market, such as REITs and commodities, were positive as well. In a notable shift this year, the office sub-sector saw a double-digit gain during the month on the back of growing leasing volume and positive sentiment stemming from a notable transaction from one of New York City’s largest office landlords.

Outlook

Year-to-date, there have been a plethora of market shaking events – a banking crisis, a debt ceiling impasse, tightening financial conditions, negative earnings growth – but July was a welcomed reprieve from the noise and markets by and large have held their ground. However, even with reasonably strong economic data being reported, there are signs of elevated potential for a slowing business cycle. As highlighted in our Mid-Year Outlook, we believe thoughtful asset allocation will be as important as ever in this environment of higher interest rates, tighter financial conditions and moderating inflation.

For more information, please contact, or schedule a meeting, with the professionals at C.W. O’Conner Wealth Advisors.

[1] U.S. Bureau of Economic Analysis. As of July 27, 2023.

[2] U.S. Bureau of Labor Statistics. As of July 12, 2023.

[3] https://www.federalreserve.gov/monetarypolicy/openmarket.htm. As of July 26, 2023.

Disclosures & Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses.

- The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

- MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

- MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country.

- Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

- Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

- FTSE NAREIT Equity REITs Index contains all Equity REITs not designed as Timber REITs or Infrastructure REITs.

- Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification.

Material Risks

- Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and over longer periods of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

- International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impact by currency and/or country specific risks which may result in lower liquidity in some markets.

- Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

- Private Equity involves higher risk and is suitable only for sophisticated investors. Along with traditional equity market risks, private equity investments are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility and/or the potential loss of capital.

- Private Credit involves higher risk and is suitable only for sophisticated investors. These assets are subject to interest rate risks, the risk of default and limited liquidity. U.S. investors exposed to non-U.S. private credit may also be subject to currency risk and fluctuations.

- Marketable Alternatives involves higher risk and is suitable only for sophisticated investors. Along with traditional market risks, marketable alternatives are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility or the potential for loss of capital. Additionally, short selling involved certain risks including, but not limited to additional costs, and the potential for unlimited loss on certain short sale positions.

Download our 2025 Financial Planning Guide